The COVID-19 pandemic has resulted in a tremendous increase in the burden on healthcare organizations across the globe. According to the WHO, as of September 29, 2020, there were 33,249,563 confirmed cases of COVID-19, including 1,000,040 deaths, with the highest number of deaths in the Americas, followed by Europe and Southeast Asia.

Furthermore, due to the COVID-19 pandemic, governments across the globe have announced country-wide lockdowns as well as social distancing measures to prevent the collapse of their health systems. Shutdown measures to curb COVID-19, however, resulted in a decrease in the number of orders of biological microscopes during the three months of April–June 2020. This has further negatively impacted the quarterly revenue of leading players operating in this market.

Currently, no effective treatment for COVID-19 is available in the form of vaccines or antiviral drugs, and patients are currently treated symptomatically. According to the WHO, there are 70 vaccine candidates under development, and three candidates are already being tested in human trials. At the forefront of the COVID-19 outbreak, many researchers worldwide are engaged in the viral research of SARS-CoV-2, the virus that causes COVID-19.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=163914483

The use of HCS makes the drug development process more time- and cost-efficient. Owing to these factors, the adoption of high-content screening for toxicity studies is expected to increase during the forecast period. This, in turn, is expected to drive market growth as live cell imaging is used in HCS to identify meaningful information from complex systems such as in vitro, in vivo, and ex vivo systems.

The high price of these instruments is also a concern for several pharmaceutical companies as they require multiple HCS systems in their RD activities (thus increasing the total cost spent on these systems). In addition to the high procurement costs, the maintenance costs and several other indirect expenses increase the total cost of ownership of these instruments. This is one of the major factors limiting the adoption of live cell imaging instruments in clinical and research applications, especially in emerging countries.

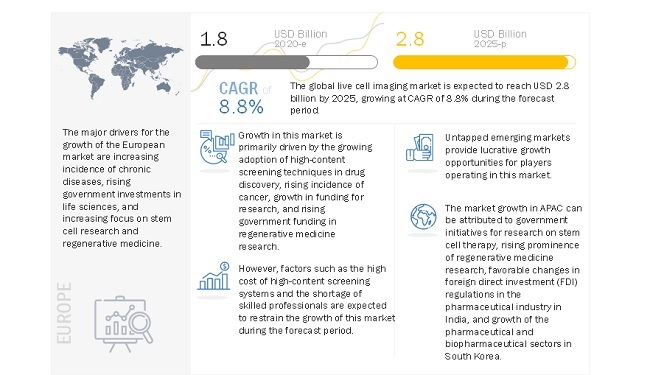

Growing adoption of high-content screening techniques in drug discovery and rising incidence of cancer primarily drives the market for live cell imaging. The growth in research funding and rising government funding and investment in regenerative medicine research will also support the market growth in the coming years. However, the high cost of high-content screening systems is limiting the overall adoption of these products.

Running live cell imaging experiments successfully can be a major challenge. The conditions under which cells are maintained under microscopes decide the success or failure of the experiment. Therefore, maintaining living cells on slides is the most crucial part of the experiment. The cells used in experiments should be in good condition and function normally under a microscope in the presence of synthetic fluorophores or fluorescent proteins.

Geographically, the global live cell imaging market is segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East Africa. Asia Pacific is expected to show the highest growth rate during the forecast period. The high growth rate of this region can mainly be attributed to the factors such as the government initiatives for research on stem cell therapy.

Based on end user, the live cell imaging market is segmented into pharmaceutical biotechnology companies, academic research institutes, and contract research organizations (CROs). In 2019, pharmaceutical biotechnology companies segment accounted for the largest share of the live cell imaging market. The large share of this segment can be attributed to the increasing RD activities and the patent cliff of various blockbuster drugs.